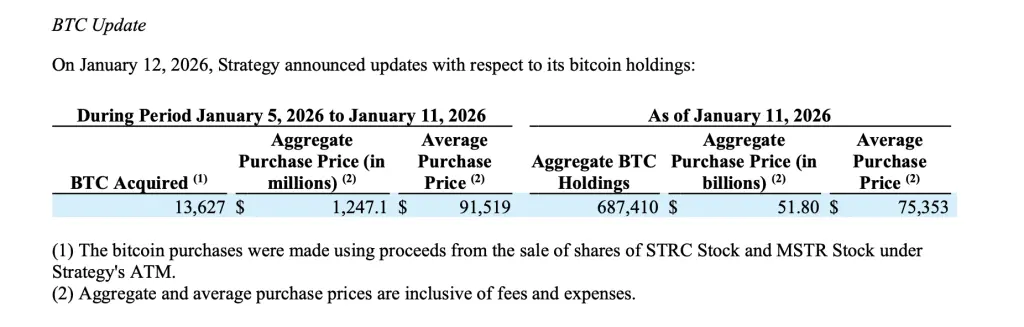

MicroStrategy purchased 13,627 Bitcoins from January 5 to 11, spending $1.25 billion at an average price of $91,519 per Bitcoin. The holdings now total 687,410 coins, with a total cost basis of $51.8 billion and an average cost of $75,353. Funds came from the sale of STRC preferred shares ($119.1 million) and MSTR common shares ($1.13 billion). There is still an issuance capacity of over $40 billion available for further purchases.

Breakdown of the $1.25 billion funding source for the buy

(Source: MicroStrategy)

Between January 5 and 11, MicroStrategy acquired an additional 13,627 Bitcoins, costing approximately $1.25 billion, with an average purchase price of $91,519 per Bitcoin, including fees and expenses. This acquisition further consolidates the company’s position as the world’s largest Bitcoin holder and continues its long-term strategy of accumulating digital assets through capital market activities.

Documents show that the funds for these Bitcoin purchases came from proceeds from the company’s stock sales via the at-the-market (ATM) program, including common and preferred shares. During the same period, MicroStrategy sold 1,192,262 shares of STRC (a floating-rate, perpetual, deferred preferred stock series A), netting $119.1 million. Additionally, the company sold 6,827,695 shares of MSTR Series A common stock, netting $1.13 billion. The total of approximately $1.249 billion exactly covers the cost of this Bitcoin purchase.

The ATM (At-The-Market) plan is a flexible equity financing tool that allows a company to sell shares gradually at current market prices rather than issuing a large block all at once. The advantage of this approach is that it minimizes market impact and avoids depressing the share price due to a sudden influx of stock. MicroStrategy has repeatedly used this method to fund Bitcoin acquisitions, demonstrating market acceptance of its strategy.

Breakdown of MicroStrategy’s multi-layered financing structure

STRC Preferred Shares: Floating-rate, perpetual, deferred, offering fixed dividends but no voting dilution

MSTR Common Shares: Direct dilution of existing shareholders but with maximum flexibility

ATM Program Execution: Gradual sale at market prices to avoid sharp declines in share price

During this period, the company’s other preferred stock issuances (including STRF, STRK, and STRD) did not involve any share sales, despite having remaining issuance capacity. This selective use of different financing tools reflects MicroStrategy’s meticulous management of capital costs. Preferred shares generally have higher costs but do not dilute voting rights, while common shares dilute shareholder equity but are cheaper. Choosing the optimal financing mix under different market conditions is a core CFO skill.

Impressive holdings of 687,410 BTC and future ammunition

(Source: MicroStrategy)

As of January 11, MicroStrategy reported holding a total of 687,410 Bitcoins, with an aggregate purchase cost of about $51.8 billion. According to filings, the average purchase price for all holdings is $75,353 per Bitcoin. At the current Bitcoin price of approximately $91,000, MicroStrategy’s Bitcoin investment has an unrealized gain of about $10.7 billion, with a return on investment of roughly 21%.

This average cost is strategically significant. $75,353 means that even if Bitcoin drops to $80,000, MicroStrategy remains profitable. This cost advantage stems from the company’s long-term, continuous buying strategy starting in August 2020, accumulating in phases as Bitcoin’s price rose from $10,000 to $100,000. Compared to investors who bought in at high points in a lump sum, MicroStrategy’s average cost significantly reduces risk.

Despite recent volatile Bitcoin prices and a general pullback in digital asset investment products, MicroStrategy proceeded with this purchase, indicating continued confidence that Bitcoin is a long-term treasury reserve asset. Saylor has repeatedly stated publicly that MicroStrategy’s strategy is not to trade Bitcoin for profit but to hold it permanently as a store of value. This “buy and hold” approach shields MicroStrategy from short-term price fluctuations.

As of January 11, the company still has substantial remaining issuance capacity, including over $20.3 billion under STRK, $4 billion under STRD, $3.9 billion under STRC, and $1.6 billion under STRF. The company also retains over $10.2 billion of available capacity under its MSTR common stock plan. These issuance capacities total over $40 billion, indicating that MicroStrategy still has ample “ammunition” to continue buying Bitcoin.

This structure enables MicroStrategy to continue seizing opportunities for funding while diversifying financing into common stock and multi-layered preferred shares with different dividend features. The use of diversified financing tools reduces reliance on a single source and enhances financial flexibility. When market conditions favor issuing preferred stock, they do so; when common stock is trading at a premium, they issue common shares—always choosing the most cost-effective financing method.

Long-term arbitrage logic with an average cost of $75,353

MicroStrategy’s disclosures reinforce its stance that Bitcoin remains a core asset on its balance sheet. Although the average purchase price is well below recent market highs, the scale and pace of acquisitions show that the company is willing to deploy capital regardless of short-term volatility. Currently holding nearly 700,000 Bitcoins, its balance sheet has become one of the most concentrated institutional holdings of Bitcoin in the global market.

Compared to the current price of around $91,000, the $75,353 average cost basis provides an unrealized gain of about 21%. More importantly, this cost basis offers a significant safety margin. Even if Bitcoin retraces to $80,000 in the future, MicroStrategy remains profitable. This buffer allows the company to withstand market fluctuations without being forced to sell.

Saylor’s long-term vision is that Bitcoin’s price will eventually reach hundreds of thousands or even millions of dollars. If this vision materializes, the current purchase price of $91,519 will be extremely advantageous in hindsight. This long-term perspective enables MicroStrategy to ignore short-term volatility and continue buying at various price levels. Since 2020, MicroStrategy has bought Bitcoin at $10,000, $30,000, $50,000, $70,000, and $90,000, employing a dollar-cost averaging strategy.

However, this approach also carries risks. If Bitcoin’s price remains below $75,353 for an extended period, the value of MicroStrategy’s assets could fall below its debts and shareholders’ equity, potentially leading to credit rating downgrades or stock price crashes. The company’s mode of issuing stock to buy Bitcoin is highly effective in a bull market but may face liquidity issues in a bear market if stock prices decline sharply, limiting future financing options.