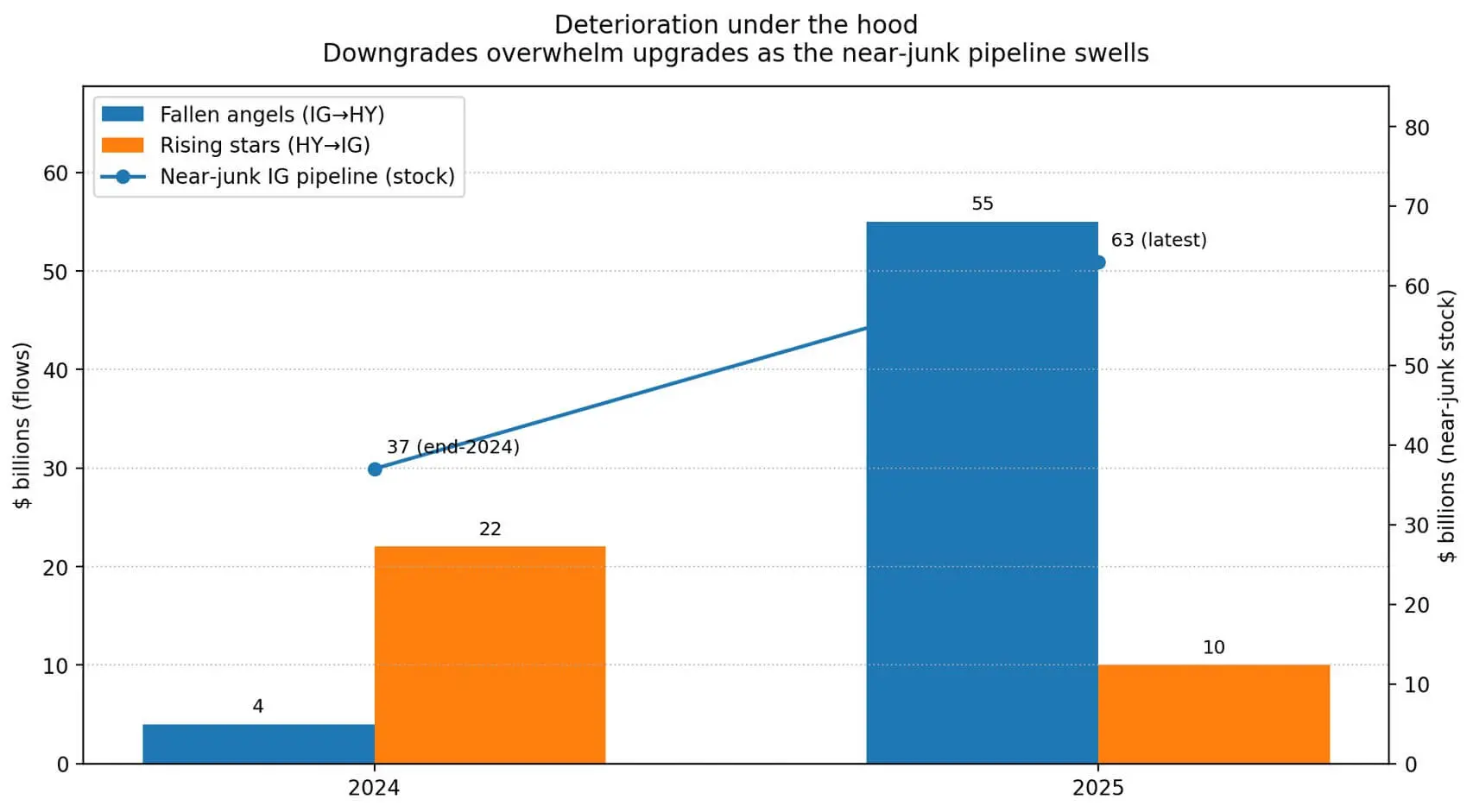

U.S. corporate credit quality is clearly weakening, even though the market appears calm on the surface. According to JPMorgan statistics, in 2025 approximately $55 billion of U.S. corporate bonds have been downgraded from investment-grade(investment-grade) to junk(junk), commonly called “fallen angels.”

Conversely, only about $10 billion of bonds have been upgraded back to investment-grade as “rising stars.” Notably, there are currently up to $63 billion of investment-grade corporate debt near the junk threshold, a significant increase from about $37 billion at the end of 2024.

However, credit spread(credit spreads) remain very low. As of January 15, data from FRED shows: investment-grade spreads at 0.76%, BBB at 0.97%, and high-yield at 2.71%.

These figures indicate that investors do not yet see this as a serious credit event, even though the “downgrade pipeline” is growing larger.

The mismatch between the silently accumulating negative risk and the subjective external sentiment is a typical context for Bitcoin to become a “convex” macro asset. Under normal conditions, slight widening of spreads usually disadvantages risk assets, including Bitcoin.

However, if credit stress increases rapidly enough to force the Fed to accelerate rate cuts or implement liquidity support measures, the initial downward pressure on Bitcoin could reverse, pushing the market into a monetary regime where Bitcoin has historically benefited.

The number of downgraded corporate bonds skyrocketed to $55 billion in 2025 from $4 billion in 2024, while the amount of upgraded bonds sharply declined from $22 billion to $10 billion.## Internal System Weaknesses

The number of downgraded corporate bonds skyrocketed to $55 billion in 2025 from $4 billion in 2024, while the amount of upgraded bonds sharply declined from $22 billion to $10 billion.## Internal System Weaknesses

The relationship between Bitcoin and the corporate credit market is highly dependent on the state of the market.

Academic research published on Wiley in August 2025 shows a negative correlation between crypto yields and credit spreads, with a significantly stronger linkage during tense market periods.

This structure explains why Bitcoin often declines when spreads start to widen but recovers strongly if the widening is large enough to alter policy expectations. The initial phase involves tightening financial conditions and weakening risk appetite.

The second phase increases the likelihood of monetary easing, with real yields falling and the USD weakening—factors that matter much more for Bitcoin than internal crypto market news.

Bitcoin is particularly sensitive to the story of monetary liquidity, not just within crypto narratives. Therefore, the “fallen angel pipeline” becomes a very important watchlist.

When corporate bonds are downgraded from investment-grade, they trigger forced selling waves from investors bound by regulations or bylaws, such as insurance companies, high-quality bond funds, or index funds. At the same time, market makers demand wider spreads to hold risk.

ECB financial stability studies show that fallen angels not only depress bond prices and worsen issuance conditions for related companies but can also spill over into stock markets and volatility.

Bitcoin often “feels” this contagion effect through similar high-beta channels: tightening financial conditions, reduced leverage, and risk-off sentiment.

But the story doesn’t end there. If credit deterioration becomes significant at the macro level, threatening corporate refinancing ability or systemic risk, the Fed has a precedent for intervention.

On March 23, 2020, the Fed launched two programs, PMCCF and SMCCF, to support the corporate bond market. BIS studies show that just announcing these programs helped spreads narrow significantly, mainly by compressing credit risk premiums.

For Bitcoin, these “balance sheet” style support measures represent a change in liquidity regime—something crypto traders often price in ahead of, or even earlier than, traditional markets.

Non-Credit Asset Perspective

The weakening of credit highlights a key fact: corporate debt always carries default risk, maturity risk, and downgrade cycles. Bitcoin does not have these features. It has no issuance cash flow, no credit rating, and no refinancing schedule.

In a context where investors reduce credit risk, especially as yields fall and USD weakens, Bitcoin can benefit on the margin as a non-credit risk asset.

This is not an “safe haven” argument, because Bitcoin’s volatility makes that interpretation misleading. It’s a capital flow argument: when credit becomes problematic, non-credit risk assets can attract capital, despite other risks.

The correlation between Bitcoin and USD is cyclical and unstable, so the “USD weak = Bitcoin up” channel is not always reliable.

However, in scenarios where credit stress drives U.S. yields down and forces the Fed to pivot policy, USD could weaken alongside falling real yields—and this macro combination has historically been highly supportive for Bitcoin.

When Subjectivity Breaks

Currently, the market is in a rather unusual state. Investment-grade spreads at 0.76% and high-yield at 2.71% remain very low historically, while the junk-bound bond market is at its largest since 2020.

From this, three main scenarios emerge, each with different implications for Bitcoin.

In the “slow bleed” scenario, spreads gradually widen without sudden jumps. High-yield could increase by 50–100 basis points, BBB by 20–40 basis points, with financial conditions tightening slowly. The Fed maintains a cautious stance, and Bitcoin moves like a risk asset, struggling when liquidity worsens without a policy pivot. This is the most common scenario and usually neutral or negative for Bitcoin.

In the “credit shakeout” scenario, spreads are repriced to levels that alter policy dialogue but do not cause a full-blown crisis. During the April 2025 stress, high-yield reached around 401 basis points, and investment-grade about 106 basis points. These levels are not yet crisis levels but are enough to make the Fed reconsider its path. If government bonds rally due to safe-haven flows and markets price in earlier rate cuts, Bitcoin could shift from risk-off to liquidity-on faster than stocks. This is a “convex” scenario: sharp decline initially, then early recovery as policy shifts.

In the “credit shock” scenario, spreads widen to crisis levels, forced selling spreads across markets, and the Fed must deploy liquidity tools. Bitcoin becomes highly volatile on both sides: plunging with the market, then surging when liquidity expectations reverse. The 2020 pattern is a prime example: Bitcoin fell from around $10,000 to $4,000 in March, then surpassed $60,000 within a year after the Fed injected massive liquidity.

The positive case for Bitcoin amid worsening credit is not about avoiding the initial shock but about benefiting from the subsequent policy response.

What to Watch

Indicators to determine when credit stress shifts from a drag to a driver for Bitcoin are relatively clear. High-yield and BBB spreads are front-line: if BBB widens faster, the market is beginning to price in fallen angel risk.

CDX IG and CDX HY indices provide clearer sentiment signals. U.S. real yields and the USD are key cross-checks: rising real yields and a strong USD are the most adverse combination for Bitcoin, while falling real yields signal potential policy pivoting.

Liquidity “pipelines,” such as Fed programs, balance sheet expansions, or repo operations, are also crucial, as stablecoins and on-chain liquidity react quickly to monetary shocks.

The credit market currently signals both positive and warning signs. January started with large investment-grade issuance and low risk premiums, indicating investors do not yet see this as a 2020-like scenario.

But the $63 billion near-junk bonds are still on the table.

If spreads remain controlled, Bitcoin’s benefit from credit stress remains hypothetical. If spreads widen, the order of events will matter most: the initial tightening, followed by expectations of easing.

Bitcoin’s bullish case amid credit deterioration is not about avoiding the first shock but about capitalizing on the second phase faster than assets still tightly linked to corporate cash flows and credit ratings.