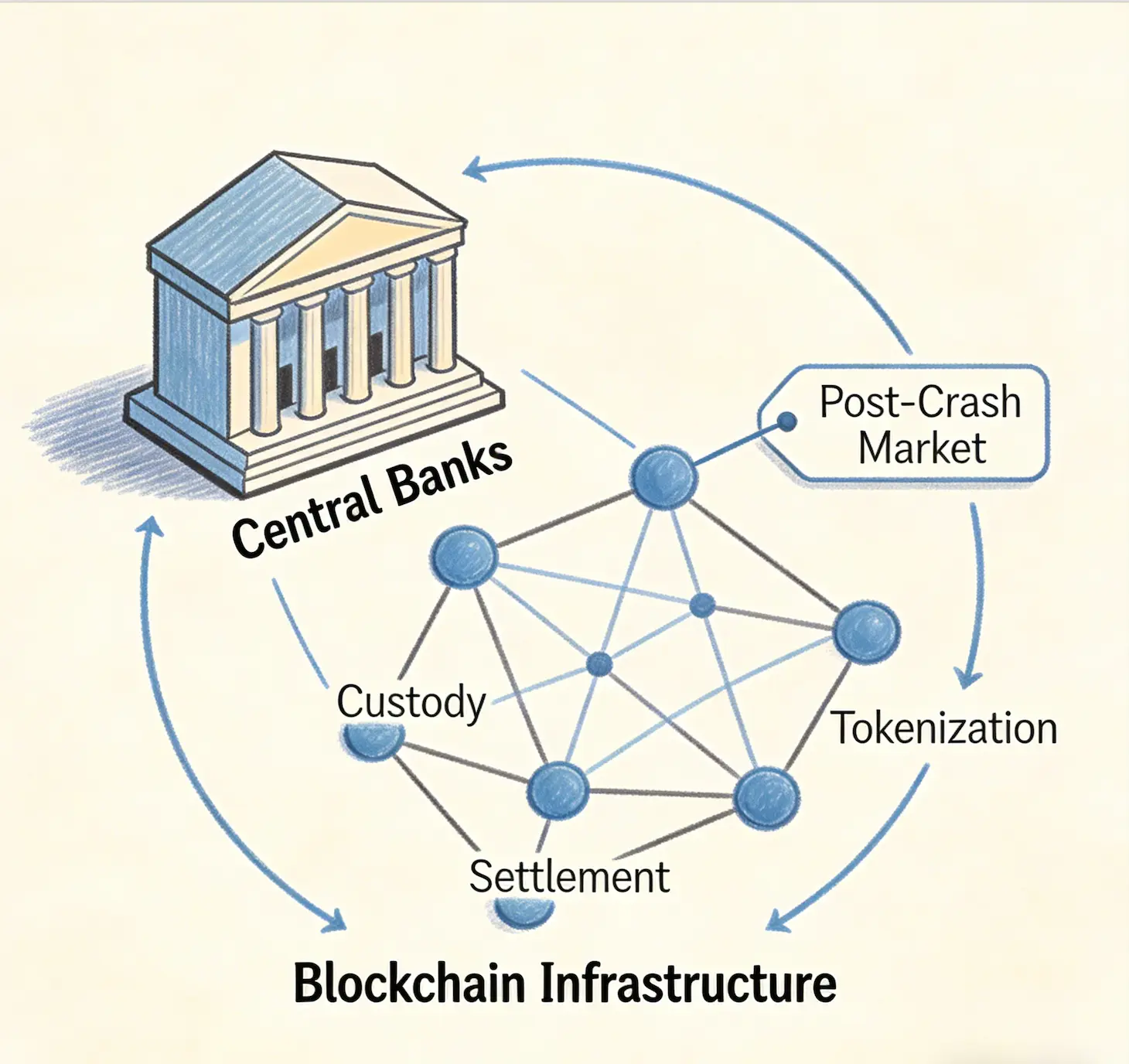

Global central banks are quietly acquiring blockchain infrastructure developed by the private sector—including custody solutions, settlement protocols, and tokenization platforms—at valuations that reflect the post-crash crypto market, according to analysis published on April 6, 2026.

Global central banks are quietly acquiring blockchain infrastructure developed by the private sector—including custody solutions, settlement protocols, and tokenization platforms—at valuations that reflect the post-crash crypto market, according to analysis published on April 6, 2026.

The Bank for International Settlements (BIS) mBridge project, a cross-border CBDC settlement platform involving China, Hong Kong, Thailand, and the United Arab Emirates, is built on an Ethereum Virtual Machine-compatible blockchain using Solidity smart contracts, while the Bank of Israel’s digital shekel project has audited technology from Israeli firms including Fireblocks, PayPal, COTI, and QEDIT without paying the full sunk costs of their research and development.

BIS mBridge Project Leverages Ethereum Technology Developed with Private Capital

The mBridge project, a cross-border central bank digital currency (CBDC) settlement platform, is built on a blockchain fully compatible with the Ethereum Virtual Machine (EVM). Its smart contracts are written in Solidity, Ethereum’s programming language, and its original consensus mechanism, HotStuff+, was developed by VMware Research with academic collaborators from Cornell and Duke universities. The entire Ethereum ecosystem’s tooling—auditing frameworks, developer libraries, and security protocols—can plug directly into mBridge without modification.

Central banks did not pay for the development of this infrastructure. The venture capitalists and token holders who funded Ethereum’s development, many of whom are now underwater or bankrupt, bore the cost. The BIS calculates that over $1.8 trillion dissolved across the Terra/Luna and FTX episodes alone. Venture capital investment in crypto firms plummeted from $32 billion in 2021 to under $10 billion by 2023. However, the underlying distributed ledger technology, smart contract architectures, and cross-border payment rails survived intact, and central banks are now acquiring them at distressed valuations.

Bank of Israel Digital Shekel Project Audits Private-Sector Technology without Compensating R&D Costs

The Bank of Israel is following a similar pattern. In 2024, the Bank ran a Digital Shekel Challenge featuring fourteen participants, including Fireblocks, PayPal, COTI, and QEDIT—Israeli-founded firms whose intellectual property and research and development were effectively auditioned for sovereign use. The Bank of Israel is an official observing member of the mBridge project, watching and absorbing the architecture that private-sector capital built.

The March 2025 preliminary design document for the digital shekel was described as “technology agnostic,” a designation that in practice means the Bank will select from whatever the private sector has built once it has seen what works. Project lead Yoav Soffer has described the digital shekel as “central bank money for everything.” The Bank of Israel’s research and development budget for the project is effectively subsidized by the private sector.

Israeli firms were pioneers in blockchain security, zero-knowledge proofs, and decentralized identity solutions. Tel Aviv produced some of the most sophisticated smart contract auditing firms in the world. However, the Bank of Israel is poised to harvest the fruits of this innovation ecosystem without paying anything remotely resembling the sunk cost. Fireblocks and StarkWare were both valued at $8 billion at their peaks, and Bancor’s record-breaking $153 million initial coin offering in June 2017 briefly held the title of largest token sale in history.

Central Banks’ Infinite Time Horizon Creates Moral Hazard for Private Innovation

Central banks possess a unique advantage: they can wait. They are not subject to quarterly earnings calls, redemption requests, or margin requirements. Their time horizon is effectively infinite. They can observe private-sector experimentation at a safe distance, knowing that whatever useful innovations emerge from the chaos, they can replicate once the dust settles and developers are too depleted to object.

While much of the relevant technology is open-source—Ethereum’s code is public, Solidity is permissionless—the years of stress-testing, security audits, regulatory navigation, and enterprise integration were not free. The open-source code is the skeleton; the muscle and sinew of production-grade systems were paid for by private capital. Central banks are not adopting a concept; they are adopting a production-grade system and paying nothing for the proving.

If every central bank pursues the same approach—waiting for the private sector to solve hard problems, then appropriating the solutions—the incentive structure for future innovation collapses. This is moral hazard in reverse. In the 2008 financial crisis, the concern was that bailing out banks would encourage reckless risk-taking. In the crypto context, the concern is that systematic appropriation by sovereigns will discourage risk-taking altogether.

Implications for Israel’s Fintech Ecosystem

For Israel, this carries a specific strategic implication. The country’s fintech and blockchain ecosystem represents not merely commercial value but a form of national technological capital. If central banks globally continue to absorb crypto infrastructure at distressed prices, venture capital that sustains Israeli firms may begin to redirect toward sectors where the fruits of innovation cannot be so easily appropriated by sovereigns. Israel’s competitive advantage in financial technology could erode not because of any failure of ingenuity, but because returns to that ingenuity are being systematically captured by the very institutions the technology was designed to disintermediate.

The analysis suggests that the Bank of Israel should structure the digital shekel not as an exercise in technology adoption but as an exercise in technology partnership. This could include equity stakes or long-term licensing agreements with Israeli firms whose R&D underpins the architecture, a sovereign innovation fund modeled on Singapore’s approach that recycles some of the value captured by the CBDC back into the domestic ecosystem, and a governance framework commitment that Israeli-developed technology will not simply be extracted and replicated without attribution or remuneration.

FAQ

What blockchain infrastructure are central banks acquiring at distressed valuations?

Central banks are acquiring custody solutions, settlement protocols, and tokenization platforms that were developed by the private sector during the crypto boom. The BIS mBridge project is built on Ethereum Virtual Machine-compatible technology, and the Bank of Israel’s digital shekel project has audited technology from Israeli firms including Fireblocks, COTI, and QEDIT.

How much value was destroyed in the crypto crash that enabled this acquisition?

Global crypto market capitalization collapsed from $3 trillion to $800 billion between November 2021 and the end of 2022, a loss of $2.2 trillion. The BIS calculates that over $1.8 trillion dissolved across the Terra/Luna and FTX episodes alone. Venture capital investment in crypto firms fell from $32 billion in 2021 to under $10 billion by 2023.

Why does this create a moral hazard for future innovation?

If central banks systematically wait for the private sector to solve hard problems and then appropriate the solutions at no cost, rational entrepreneurs may reduce investment in financial infrastructure. The concern is that the expected outcome of state appropriation will discourage risk-taking, potentially eroding the competitive advantage of innovation hubs such as Israel’s fintech ecosystem.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.