Why Crypto is becoming Fintech and Fintech is becoming Crypto

Crypto or blockchain is a permissionless, global rail where people can hold, transfer, purchase/sell, lend/borrow, and utilize their assets however they want anywhere in the world.

You hold your own funds (self-custody) and you interact with services or applications in a way where you’re still holding your own funds.

This is contrary to traditional finance system where banks (physical/neobank) custody your funds and provide banking services to you.

The fluidity nature of the blockchain rail make it a perfect setup for institutions looking to move capital around, enterprises looking expand payment rails via stablecoins, or retail looking to invest/optimize their assets.

In this article, we’ll explore the shift from Defi to Fintech and Web2/Web3, the role of AI, the transformation within the industry and the opportunities that come with it.

Let’s dig in ↓

Let me tell you about about the fintech playbook of Grab, one of the most dominant ride-hailing / super-app player in Southeast Asia.

Grab started out offering ride hailing in Malaysia with the goal to make taxi safer & more reliable. The platform got popular in Malaysia and expanded to PH, TH, SG, and VN.

Grab did not just build a taxi app BUT a trust platform in a region w/ limited infra and fragmented transport systems.

Grab then expanded the services to cover private cars, motorbikes, food delivery, parcel delivery, and in-app payment system (wallet). All services using the same app, drivers, and payment rails, forming super app eco.

Grab realized that the wallet/payment rails (GrabPay) is the payment infra that glues everything together (users pay for rides & deliveries, store value & transact with merchants, drivers & riders use it to store/spend, financial data & transaction behaviors are captured)

The payment infra serves as foundation for Grab to partner with lending & insurance startups to offer financial products to drivers (micro loans, insurance).

Now GrabPay has grown into major regional e-wallets with more integrations & financial services (more embedded finance, merchant loans, drivers loans using in-app credit scoring, partnerships with banks & telcos for financial products)

You get the idea.

tl;dr of Grab playbook

- Establish the trusted platform with large userbase on both demand & supply side (users, drivers, merchants/vendors)

- Connect everything with payment rails/wallet infra and acquire financial & spending data

- Structure embedded financial products for the userbase based on the data

- Grab is now a fintech company embedding finance deeper: savings, investments, insurance, BNPL, and digital banking

Ride-hailing, food delivery ➔ Fintech

Crypto <-> Fintech

We’re starting to see Grab-like playbook with both Web3 projects and Web2 companies i.e. Crypto becoming Fintech while Fintech becoming more Crypto

Why?

Crypto TAM (rev generated from services/apps) is tiny vs Fintech TAM so it makes a lot of sense to bring crypto value prop (Defi, tokenization, stablecoin, lending/borrowing, yields) to broader consumers.

Traditional rails still have that friction with investing, saving, accessing banking services, and in a lot of cases users need to trust service providers to hold their funds for them. Crypto/blockchain is the perfect solution for this.

2 Case Studies

1. EtherFi (Crypto ➔ Fintech)

@ ether_fi started out as liquid restaking provider during the @ eigenlayer restaking szn back in 2023 providing restaked ETH and composable Defi vault strategies that deploys eETH, weETH, and stables into defi strategies to maximize return. The team focused on growing liquidity and composability of the strategies

In 2025, Etherfi signaled a shift towards offering banking-like services & fintech features, blending Defi with everyday financial use cases — spend, save, earn linking crypto & fiat, bill payments, and payroll services.

The feature that enabled more mainstream adoption was Visa Cash card that allows users to directly spend their crypto or use their crypto as collateral to borrow stables and spend (without selling your assets). The ~3% cashback, token incentives, Apple Pay/Google Pay, and non-custodial nature of the card attracted a lot of users & volume to their platform (and to their vault products) i.e. more people park capital on EtherFi vaults

Etherfi is positioning to be a Neobank that brings Defi value to normal, mainstream users. Who wouldn’t want an ability to seamlessly borrow stables to spend or earning ~10%+ interests on their stables

2. Stripe (Fintech ➔ Crypto)

@ stripe started off providing simplified payments infrastructure for devs and online businesses back in 2010. Stripe provides clean APIs for merchants to accept payments, manage subscriptions, fraud, payouts, and embed financial services (solving all the massive hassles for any merchants)

Over time Stripe expanded to full stack financial infra platform, providing modular APIs and products that let any company build, embed, and scale financial services without becoming a bank

- Stripe Connect: marketplaces to pay third-party sellers, drivers, creators globally, handling complex KYC and compliance behind the scene

- Stripe Billing automated subscription system/backbone for SaaS

- Stripe Treasury: embedded finance (store money, banking services)

- Stripe Issuing: create and manage physical or virtual cards instantly

- Stripe Radar integrated machine-learning-driven fraud detection

Stripe slowly test out crypto rails and acquires major infra players, acquiring Bridge (stablecoin payment infra), Privy (crypto wallet/onboarding infra), and then announced a full-on push to own its rails by developing a payments-first L1 (Tempo)

Stripe is positioning to become the foundational layer for next-gen global payments, unifying fiat + stablecoins + onchain rails under a single developer platform i.e. programmable, borderless money any time any where

What does all of this mean?

Beyond these two players, there are a lot more players trying to capture the pie (from both Crypto to Fintech and Fintech to Crypto).

What it essentially means is that Defi & TradFi, Web2 rails & Web3 rails are converging and blockchain is becoming the backbone infrastructure powering real-world economies.

Defi TVL could go 10x from $174bn to $1.74tn in the next 5 years. There are $140tn in wealth management, assuming ~1% of that is parked in Defi seems pretty possible.

Stablecoins could ended up powering general apps & platforms behind the scene (regardless of issuer) while offering yields to users.

Spot, perps, prediction markets becoming more mainstream as the value prop of trading crypto, tokenized stocks, on-chain commodities, and any assets (events, politics, macro, Taylor Swift) is massive. Every enterprise will want to own these user funnels themselves.

Because of the sector convergence, enterprise sales & strategies targeting normal retail will be a necessity

Crypto “projects” will need to become “startups”. Degeness toned down, professionalism dialed up + trust needs to be built.

As builders, you’ll need to sell your Defi platforms to enterprises, integrating your defi vault products into Fintech apps or wealth management platform. You’ll need to form enterprise sales team, understand how to sell it to them, risk/compliance and security will be key for their decision making process.

We’re starting to see initial examples of this where crypto-native teams go way beyond CT

- @ Polymarket getting investment from NYSE parent co (valuing Polymarket at $9mn post-market), extending prediction markets to TradFi and setting the stage for the entire prediction market industry

- @ flock_io partnering with governments, banks, international institutions, and listed companies to enable privacy-preserving domain-specific AI. Dedicated team at Flock tackling traditional industries/capital markets.

- @ pendle_fi working to onboard TradFi/Wallstreet into on-chain interest rate products — KYC-based, permissioned pools

- @ Mantle_Official launching UR Global Neobank “world’s first blockchain-based neobank”. Unified multi-asset account (via Swiss-backed IBAN accounts), Mastercard debit card w/ SWIFT, SEPA, SIC and L1/L2s for easy on-off ramp, self-custodial, and upcoming Defi integrations (yields on idle balance, Mantle-native defi products)

- @ useTria originally started with BestPath, AI-optimized solver network that find best route for swaps across EVM, SVM, and other VMs (Sentient, Talus, Polygon, and Arbitrum Orbit chains integrated). Tria has expanded to offering Neobank/Fintech services starting from cash card (users earn yields from assets and can spend altcoins directly)

- Exchanges are building embedded finance inside on-chain wallets, acting as discovery layer for all things Defi (and soon TradFi) e.g. OKX wallet, Binance Wallet, etc.

- And many more crypto teams launching crypto cards

Seems like @ CelsiusNetwork was going about it in the right direction, enabling native yields on Bitcoin, ETH, and stables, providing services like yields on deposits, collateralized loans, payments, debit card. The right vision but failed because execution, risk management, and transparency were severely lacking.

How Does Web3 AI fit in?

For the sake of simplicity, there are 3 main sides to this

- Get shit done

- Make sure you can trust the AI that gets shit done

- Get the talents to get the AI to get shit done

Get shit done

Since crypto is mostly financial use cases, AI systems that enhance Defi, predictions, and trading experience are the top use cases that Web3 AI builders are building towards to

Trading agents/co-pilots, AI-enabled dynamic Defi strategies, personalized Defi agents e.g. @ Cod3xOrg, @ Almanak__, @ gizatechxyz

Prediction AI/ML teams that predict asset prices, predict outcomes, weather, and more e.g. @ sportstensor, @ SynthdataCo, @ sire_agent

The AI and ML systems build on top of existing crypto verticals (primarily Defi), enabling better accessibility, reducing complexity, improving yields and risk management.

Make sure you can trust the AI that gets shit done

You can’t blindly trust AI just like you can’t trust any human, you can’t trust the infrastructure & the human behind the AI as well. So who do you trust?

Yourself, You verify everything.

This is where verifiable infrastructure comes in

Ethereum ERC-8004 acts as the trust layer i.e the passport for AI + Google’s AP2 + Coinbase x402 act as payment system/rail (stablecoin & traditional rails) that enables agents to transact between each other or w/ other Web2 services

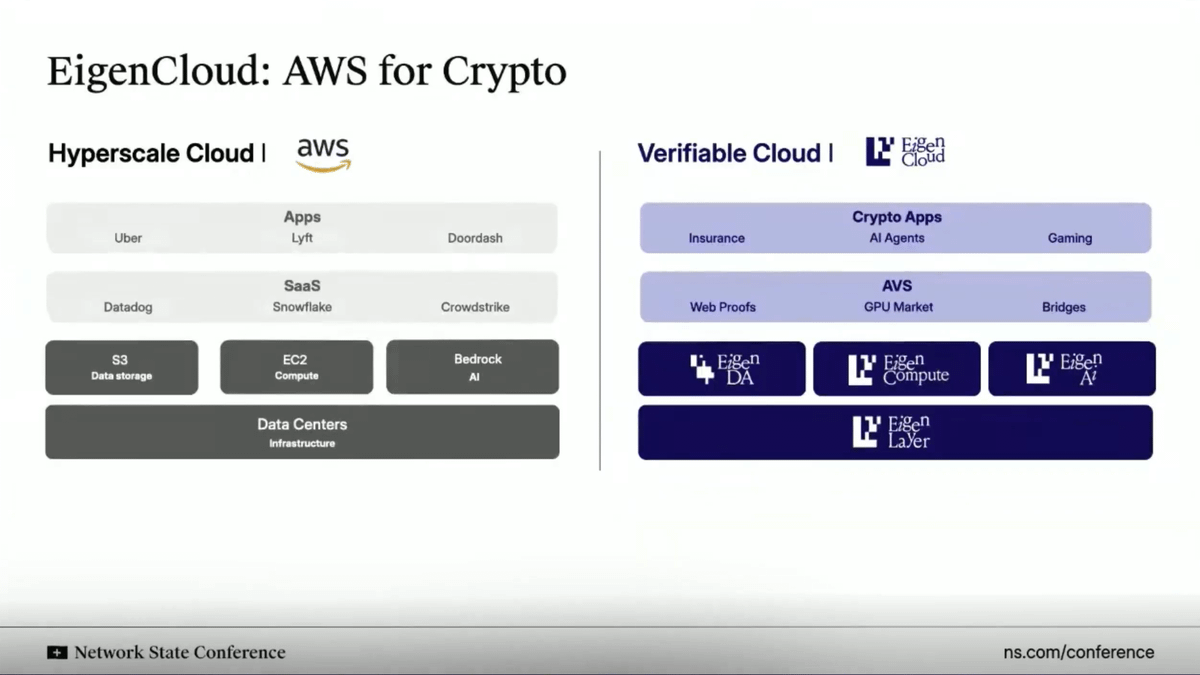

Just like AWS Cloud, @ eigenlayer is providing verifiable cloud infrastructure for everything. Instead of hosting/running everything on centralized servers, Eigen enables off-chain compute while verifying the results/inference on-chain.

The solution (EigenAI & EigenCompute) is great for AI agents/apps use cases like trading agents and Defi use cases.

Eigen has this primitive called deterministic inference, ensuring that LLMs produce identical outputs for the same inputs across repeated executions i.e. ensure they don’t hallucinate/they become deterministic.

Similar to how restaked ETH is used to vouch for smart contract, EIGEN is used to vouch/attest for AI agents/applications. Anyone can re-run the exact inference to verify inference and check whether the outputs match.

What all this enables is (i) trading agents don’t go rouge (ii) recommendation engine in social media stay consistent/tamper-proof every time (iii) autonomous agents hold funds securely as their inference can be audited/verified (essentially mitigating hallucination challenges)

Get the talents to get the AI to get shit done

AI/ML engineers are one of the most sought after resources. If you’re really good, you get poached by centralized frontier AI labs. If you’re really really good, you start one yourself.

OR you can opt to join in Darwinian AI ecosystems

These are ecosystems that offer KPI-based incentives for “miners”, “trainers” those running AI or ML models to contribute/solve a certain task. If you provide a good output that meets the objective, you earn good incentives.

Bittensor and @ flock_io are the two most well-known Darwinian AI ecosystems and miners or trainers can earn 6-7 figs in yearly incentives based on how they perform or how much stake they have within the ecosystem.

The goal of Darwinian AI ecosystems is to use incentives to attract talents, forming vibrant developer community that contribute to certain tasks. The ultimate goal is to get to the stage where revenue generated from the outputs exceed that of the incentives (financing cost paid to attract talents)

We’ve all seen how powerful this is where prediction models on Bittensor subnets outperform market benchmark or Flock delivering privacy-preserving domain-specific AI use cases to big institutions and governments like UNDP, Hong Kong, etc.

Tying it all together

Crypto, fintech, and AI are converging, forming a new financial operating system

At the heart of it is infrastructure convergence

- Crypto rails are becoming the programmable, borderless settlement layer for the internet.

- Fintech is providing the UX, compliance, and trust layers needed for mainstream adoption.

- AI is becoming the decision and automation layer that optimizes liquidity, personalization, and user experience.

Stablecoins become the invisible layer powering consumer apps, on-chain identity + verifiable compute underpin trust across AI agents/apps, traditional instos & fintech integrated Defi (or permissioned Defi) to unlock new yield opportunities, and millions of new users gain direct ownership, transparency, and global access to capital and intelligence.

Personal Note: Thanks a lot for reading! This article that you see here is a slightly shorter version (if you want my unfiltered thoughts do check out the Substack version)

And if you want to see on upcoming DeAI projects that I’m excited for, check out The After Hour series on my Substack.

Disclaimer: This document is intended for informational & entertainment purposes only. The views expressed in this document are not, and should not be construed as, investment advice or recommendations. Recipients of this document should do their due diligence, taking into account their specific financial circumstances, investment objectives, and risk tolerance (which are not considered in this document) before investing. This document is not an offer, nor the solicitation of an offer, to buy or sell any of the assets mentioned herein

Disclaimer:

- This article is reprinted from [Defi0xJeff]. All copyrights belong to the original author [Defi0xJeff]. If there are objections to this reprint, please contact the Gate Learn team, and they will handle it promptly.

- Liability Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute any investment advice.

- Translations of the article into other languages are done by the Gate Learn team. Unless mentioned, copying, distributing, or plagiarizing the translated articles is prohibited.

Share

Content

Related Articles

The Future of Cross-Chain Bridges: Full-Chain Interoperability Becomes Inevitable, Liquidity Bridges Will Decline

Solana Need L2s And Appchains?

Sui: How are users leveraging its speed, security, & scalability?

Navigating the Zero Knowledge Landscape

What is Tronscan and How Can You Use it in 2025?