USDe is designed as a crypto-native stablecoin. The protocol holds assets such as BTC and ETH, while simultaneously opening equivalent short positions in derivatives markets so that price movements offset one another. This structure sets Ethena apart from fiat-backed stablecoins and introduces a new model for stability.

In addition, Ethena introduces sUSDe as a yield-bearing version of the stable asset. Users who stake USDe can earn protocol-generated returns, primarily derived from funding rates and yield on underlying assets.

By combining a stability mechanism with a yield engine, Ethena expands the role of stablecoins beyond simple transaction tools, positioning them as income-generating onchain assets.

Overview of Ethena (ENA) and the USDe Stablecoin Mechanism

USDe is the core stablecoin of the Ethena protocol, designed to provide a stable asset without relying on traditional financial infrastructure. It achieves this through a combination of crypto collateral and derivatives hedging, often described as a synthetic dollar model.

Source: ethena.fi

USDe is backed by a mix of assets, including ETH and BTC, and may also include stablecoins such as USDC and USDT. This diversified collateral base helps improve system resilience and provides a buffer during market volatility.

USDe follows a 1:1 backing structure, but unlike overcollateralized stablecoins, its stability comes from hedging rather than excess collateral. This improves capital efficiency and allows for more flexible system design.

USDe can be used across both CeFi and DeFi environments, including lending, trading, and liquidity provisioning. This composability enhances its overall utility.

| Stablecoin Type |

Stability Mechanism |

Collateral Type |

Capital Efficiency |

| Fiat-backed stablecoin |

Bank reserves |

USD and treasuries |

High |

| Overcollateralized stablecoin |

Crypto collateral |

ETH and others |

Lower |

| Ethena (USDe) |

Delta-neutral hedging |

Spot + derivatives |

Higher |

This comparison highlights how Ethena introduces a new balance between stability and efficiency, positioning it as an innovative stablecoin model.

How the Delta-Neutral Mechanism Maintains Stability

The delta-neutral strategy is the core of USDe’s design. Its goal is to eliminate exposure to price volatility by balancing spot asset holdings with offsetting derivatives positions. Instead of relying on fiat reserves, Ethena uses financial engineering to maintain stability, making USDe a truly crypto-native stablecoin.

In practice, when the protocol holds a certain amount of crypto assets such as ETH or BTC, it simultaneously opens an equivalent short position in derivatives markets. For example, if the protocol holds $100 worth of ETH, it will open a $100 short position in ETH perpetual futures.

If ETH rises, the spot position gains value while the short position loses. If ETH falls, the short gains offset the loss in spot value. This balance keeps the overall portfolio relatively stable.

Because of this structure, USDe’s value does not depend on the direction of asset prices but on the effectiveness of the hedge. The dynamic equilibrium between spot and derivatives positions allows USDe to remain stable in both rising and falling markets.

This hedging process is typically automated. The protocol continuously rebalances positions based on price movements and funding rate changes, ensuring the system maintains its delta-neutral exposure over time.

Ethena’s Spot and Perpetual Futures Hedging Structure

Ethena’s stability model relies on the interaction between spot assets and perpetual futures positions. Spot assets provide the collateral base, while short positions in derivatives offset price risk. This dual structure enables Ethena to operate without fiat reserves.

On the spot side, Ethena primarily holds highly liquid assets such as BTC and ETH. These assets offer deep market liquidity, enabling efficient hedging and reducing slippage risk. The protocol may also hold stable assets like USDT and USDC to enhance liquidity management and system stability.

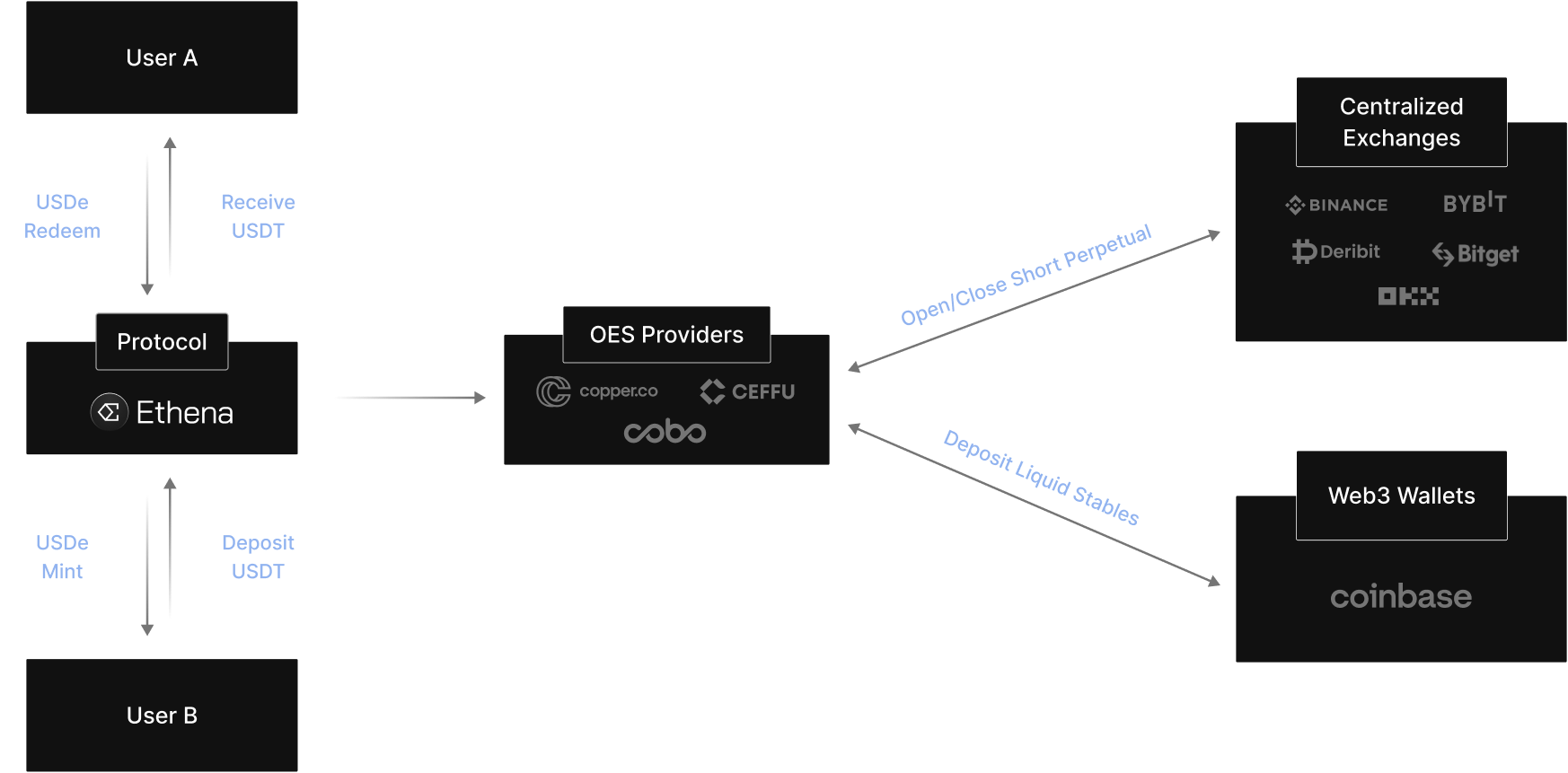

In derivatives markets, Ethena opens short positions across multiple exchanges. This multi-venue approach reduces reliance on any single platform and improves execution efficiency, strengthening overall system resilience.

Another key feature is Off-Exchange Custody. Collateral is not held directly on exchanges but stored with independent custodians. Funds are only moved when needed for margin or settlement, reducing counterparty risk.

| Component |

Role |

Risk Control Method |

| Spot assets (BTC, ETH) |

Provide collateral |

Use of high-liquidity assets |

| Short perpetual positions |

Hedge price volatility |

Multi-exchange execution |

| Stablecoin assets (USDT, USDC) |

Liquidity buffer |

Downside protection |

| Off-Exchange Custody |

Asset storage |

Reduced exchange risk |

This layered structure allows Ethena to maintain stability across different market conditions.

The Role of Funding Rates in Ethena’s Yield Model

Funding rates are a key source of income for Ethena. In perpetual futures markets, long and short traders exchange periodic payments to keep contract prices aligned with spot markets. When market sentiment is predominantly long, longs pay shorts.

Because Ethena maintains large short positions, it can collect funding payments during bullish market conditions. These payments form a major component of the protocol’s revenue and support the yield offered to sUSDe holders.

In addition, Ethena may earn yield from its spot assets. For example, staked ETH can generate staking rewards, while stablecoin holdings may produce additional returns. Combined with funding income, this creates a diversified yield structure.

In 2024 market conditions, average funding rates were approximately 11% for BTC and 12.6% for ETH. Supported by these income streams, sUSDe has at times delivered annualized yields of around 19%. This positions Ethena as a model that combines stability with income generation.

Risk Management and Stability Safeguards

Despite its design, Ethena faces several risks and relies on multiple layers of risk control.

First, automated hedging reduces exposure to price volatility. The protocol continuously adjusts positions to maintain a stable structure.

Second, a multi-exchange strategy reduces dependency on any single trading venue. If one platform encounters issues, positions can be managed elsewhere.

Third, Off-Exchange Custody minimizes asset custody risk by keeping collateral with independent providers rather than exchanges.

Finally, dynamic risk models guide system adjustments. If funding rates decline or volatility increases, the protocol may rebalance assets or reduce exposure to maintain long-term stability.

End-to-End Workflow of Ethena (ENA)

The Ethena process begins when users mint USDe by depositing collateral such as ETH or USDT through smart contracts.

The protocol then opens corresponding short positions in derivatives markets to establish a delta-neutral hedge.

During operation, the system continuously rebalances positions and collects funding rate income. These earnings are directed into the protocol’s yield pool.

Users can stake USDe to receive sUSDe and earn yield. When users redeem, the protocol closes the corresponding positions and releases the underlying collateral, completing the cycle.

Summary

Ethena uses a delta-neutral hedging strategy to create USDe, a stablecoin that does not depend on fiat reserves but instead relies on crypto assets and derivatives markets. By offsetting price movements between spot and short positions, the protocol maintains stability.

At the same time, Ethena integrates funding rates and asset yield into its design, transforming USDe into a yield-generating stable asset. This approach improves capital efficiency and expands the role of stablecoins within the crypto ecosystem.

As the market evolves, Ethena’s synthetic dollar model may represent an important direction for stablecoin innovation, helping drive the next phase of decentralized finance.

FAQ

- How does Ethena maintain stability?

Ethena uses a delta-neutral hedging mechanism by holding spot assets and opening equivalent short positions to offset price movements.

- Is USDe fully collateralized?

USDe uses a 1:1 backing model combined with derivatives hedging, rather than relying on overcollateralization.

- Where does Ethena’s yield come from?

It primarily comes from funding rates, staking rewards, and returns on stable assets.

- What is sUSDe?

sUSDe is the staked version of USDe. Users who stake USDe receive sUSDe and earn protocol-generated yield.