Futures

Access hundreds of perpetual contracts

TradFi

Gold

One platform for global traditional assets

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Introduction to Futures Trading

Learn the basics of futures trading

Futures Events

Join events to earn rewards

Demo Trading

Use virtual funds to practice risk-free trading

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

Trade on-chain assets and earn airdrops

Futures Points

Earn futures points and claim airdrop rewards

More

US-Iran "Tug-of-War" Rocks Global Markets, US Stocks Rebound, US Treasuries Surge Volatility, Crude Oil Plummets 10%, Gold Falls for Ninth Consecutive Day

Trump announces delay in strikes on Iran’s energy infrastructure, triggering sharp volatility in global financial markets on Monday. Oil prices plummet over 10%, gold recovers most of its intraday losses. U.S. stocks close higher by over 1%, but Iran immediately denies negotiations are ongoing, halting the market rally at intraday highs.

( comparison of intraday movements in US stocks, bonds, and oil)

comparison of intraday movements in US stocks, bonds, and oil)

According to CCTV News, U.S. President Trump stated on the 23rd that he has instructed a five-day pause on all military strikes against Iran’s power plants and energy infrastructure, provided ongoing meetings and discussions are successful. Subsequently, CCTV reported that Iran’s Islamic Parliament Speaker, Kalibaf, posted on social media denying any dialogue with the U.S.

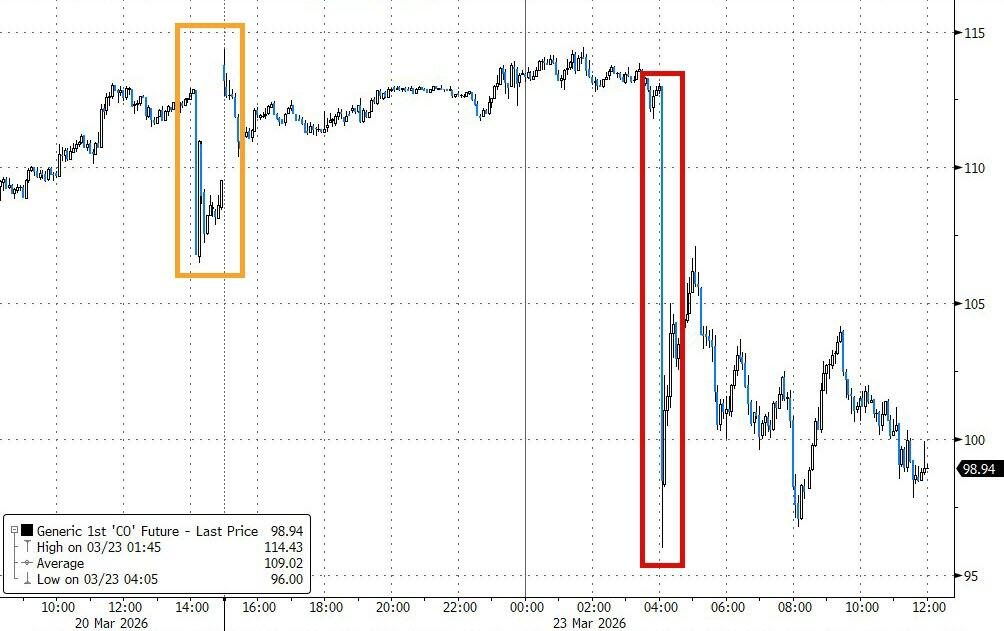

Following the announcement, Brent crude briefly fell over 14%.

( Brent crude futures briefly plunge 14%)

Brent crude futures briefly plunge 14%)

Kalibaf said that news about negotiations is “false information” aimed at manipulating financial and oil markets to help the U.S. and Israel escape their current “predicament.” His firm stance temporarily narrowed the decline in oil prices, as Chris Larkin from E*Trade noted:

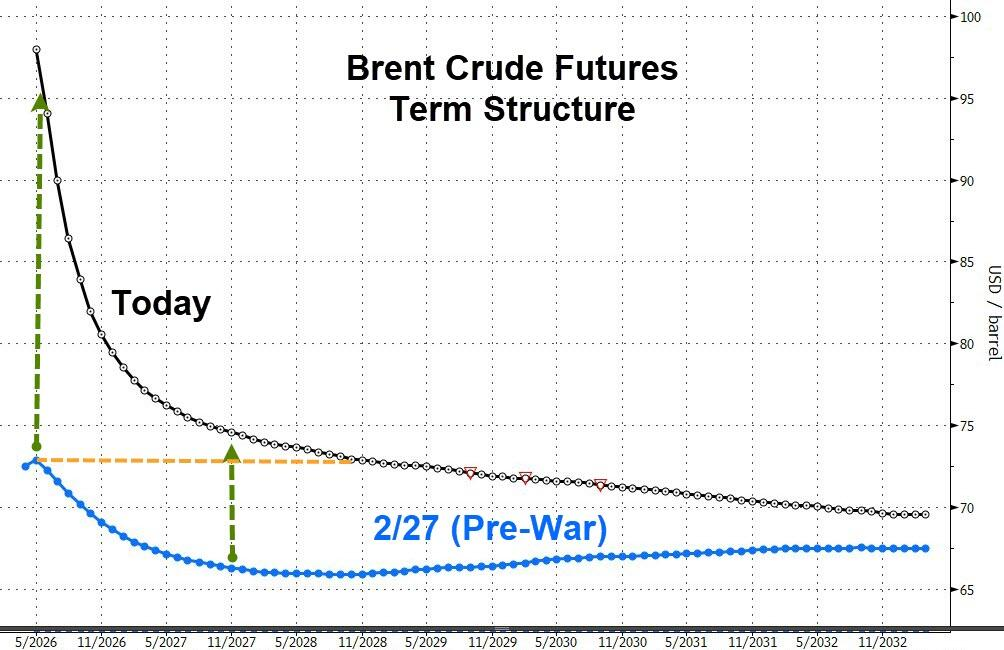

It is noteworthy that crude oil futures remain elevated and in backwardation, with current futures prices implying a return to pre-conflict levels only by November 2028.

( Brent futures term structure comparison chart)

Brent futures term structure comparison chart)

Edward Jones’ Brock Weimer pointed out that the most convincing risk-off signal would be a recovery in actual flow of oil through the Strait of Hormuz, not just verbal statements. Crossmark Global Investments’ Chief Investment Officer Bob Doll said:

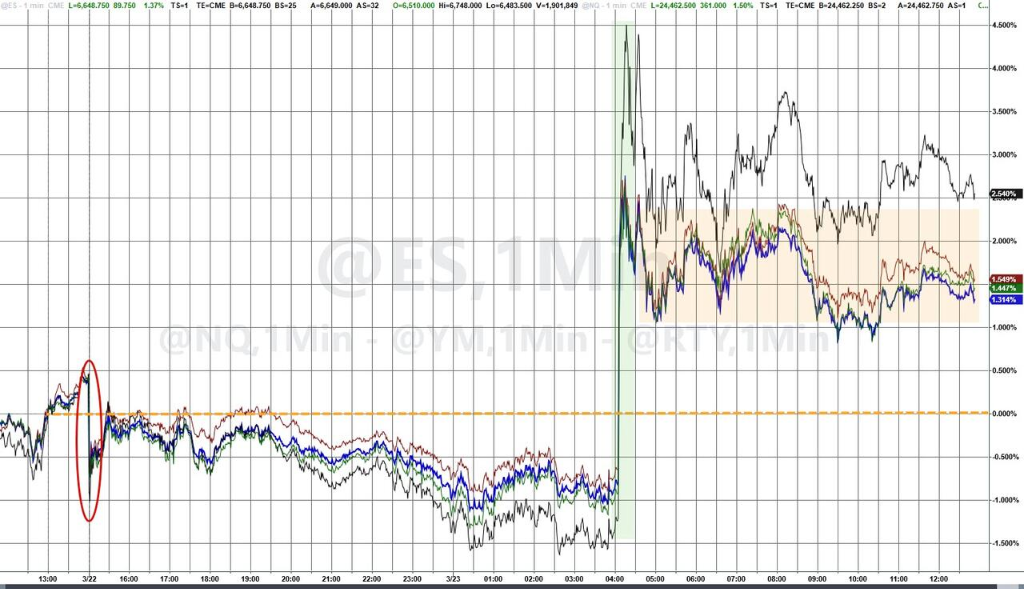

On Monday, all three major U.S. stock indices closed higher, with the Dow soaring nearly 1,000 points at one point. After Iran’s Foreign Minister denied the reports, U.S. stocks retreated from intraday highs.

( Intraday movements of major U.S. stock indices)

Intraday movements of major U.S. stock indices)

Goldman Sachs trader Rich Privorotsky noted that Trump’s behavior over the past 72 hours follows a fixed pattern: releasing a “considering tightening” signal on Friday, escalating to the toughest stance on Saturday, and announcing a “pause for five days” on Monday. This sequence creates tension, sets a deadline, then offers a de-escalation to generate internal political gains.

Former U.S. Department of Defense Middle East Deputy Assistant Secretary Dana Stroul said that Trump’s move appears more like seeking a stepping stone. If he actually attacks Iran’s civilian energy infrastructure, it could constitute a war crime. The timing of the five-day pause announcement, just before U.S. markets open, is “no coincidence.”

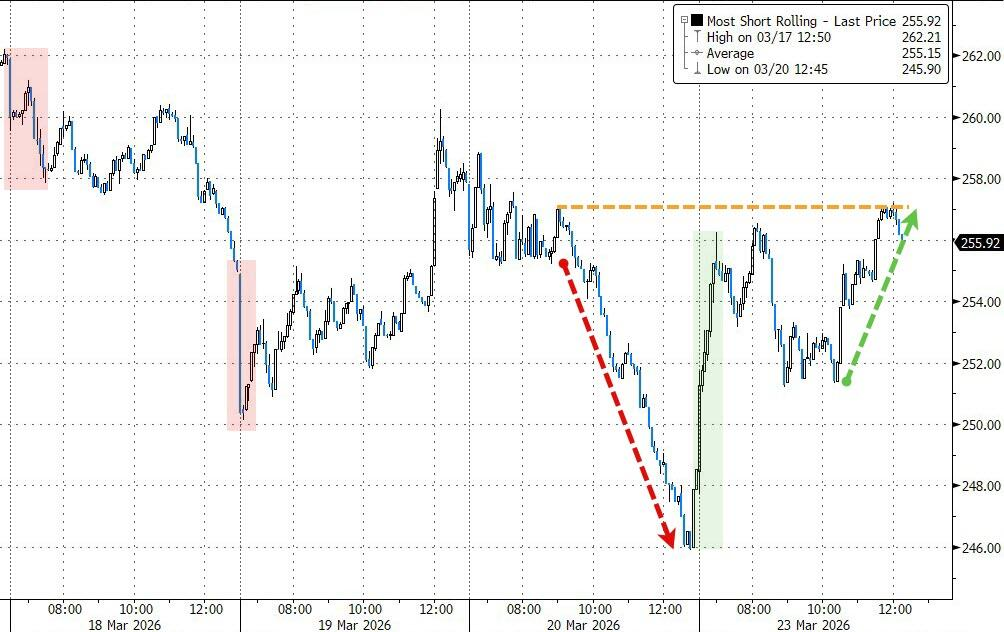

Additionally, analysts believe that much of Monday’s stock rally was driven by short covering rather than new long positions. Goldman Sachs’ trading desk activity scored only 3 out of 10, with ETFs being the main driver.

( Market sentiment reversal: short sellers forced to cover, quickly recoup last Friday’s losses)

Market sentiment reversal: short sellers forced to cover, quickly recoup last Friday’s losses)

According to data from Bespoke Investment, before this week, over 50% of S&P 500 components were in “oversold” territory, with only 5.4% in “overbought,” the most extreme since last April’s tariff turmoil. Scott Rubner of Citadel Securities noted that the current short position levels in U.S. stocks are historically rare, saying:

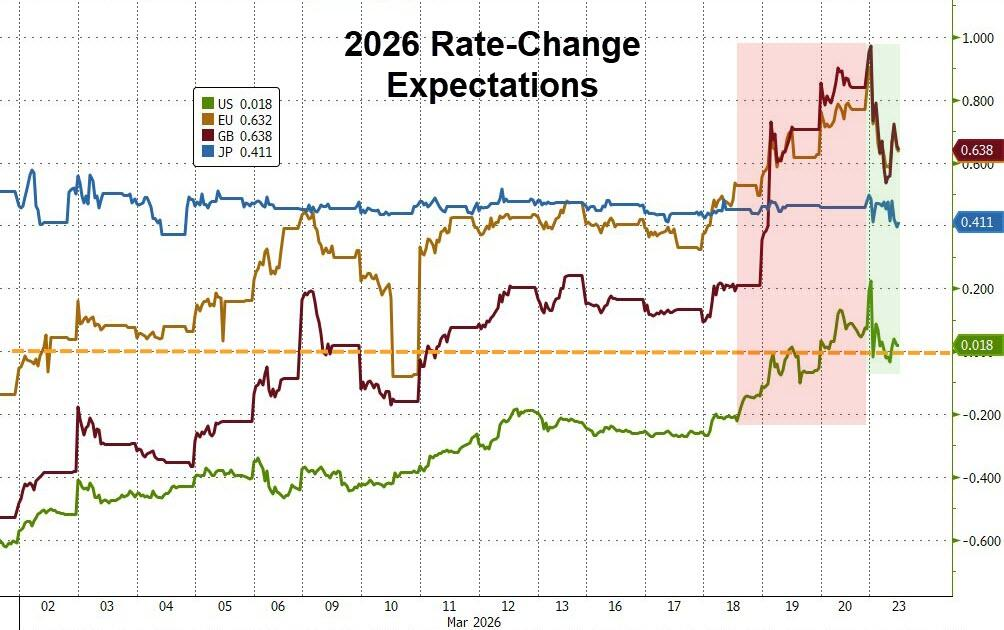

However, Bloomberg macro strategist Michael Ball warned that the Monday rebound in the S&P 500 does not change the core issue: rising oil prices boost inflation expectations, which may keep the Federal Reserve on hold and tighten financial conditions.

( Comparison of rate cut expectations in the U.S., Europe, UK, and Japan this year)

Comparison of rate cut expectations in the U.S., Europe, UK, and Japan this year)

From a technical perspective, this rebound merely pulls the indices back to the middle of their recent downtrend, with the S&P 500 still below its 200-day moving average, the Nasdaq down about 3% from pre-conflict levels, and the Dow down approximately 5.5%.

( Overall, the S&P 500 rebounds to the middle of the downtrend channel, still below the 200-day moving average)

Overall, the S&P 500 rebounds to the middle of the downtrend channel, still below the 200-day moving average)

Falling oil prices have driven U.S. Treasury yields lower, with market expectations for Fed policy adjusting marginally. The 10-year Treasury yield fell 2 basis points today, the 2-year yield down about 3 basis points, with traders slightly reducing last week’s hawkish bets, leaving room for several basis points of rate cuts this year.

( )

)

The dollar index sharply declined by 0.5%, with the euro rising to 1.1613 USD, and the pound up 0.7% to 1.3430 USD. However, cross-currency basis swaps indicate that dollar funding demand remains high, and dollar liquidity pressures have not eased, warranting ongoing attention.

( Dollar index decline)

Dollar index decline)

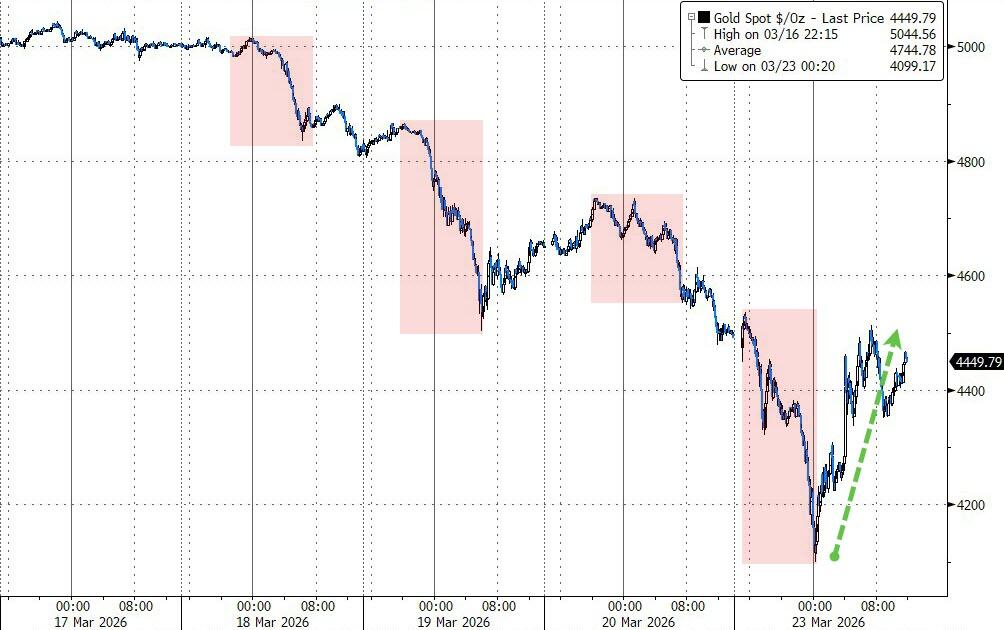

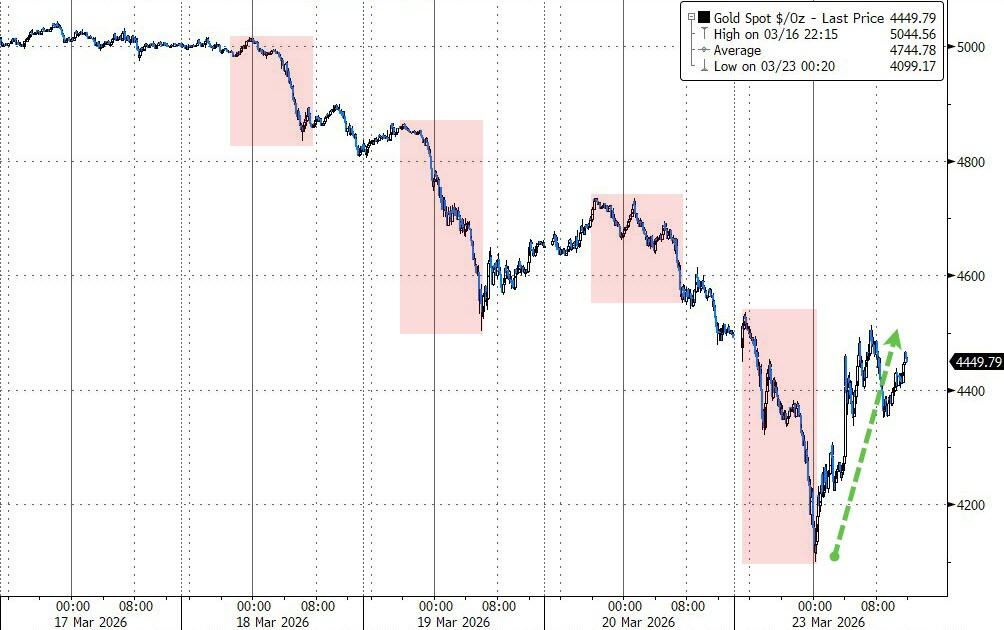

Precious metals showed unusual volatility. Spot gold fell about 2% to around $4,400, briefly rebounded but failed to hold gains, down roughly 27% from January highs.

( Gold price rebound)

Gold price rebound)

Goldman Sachs’ Rich Privorotsky believes that the recent four consecutive days of decline in overnight gold trading are driven less by fundamentals and more by sovereign fund reserve liquidations, speculative long unwinds, and leverage de-leveraging.

Industrial metals like silver and copper recovered intraday losses, closing slightly higher. Analysts see industrial metals as a barometer of global economic health, with overnight risk appetite improving.

( Despite declines in gold and platinum today, silver and copper rebounded)

Despite declines in gold and platinum today, silver and copper rebounded)

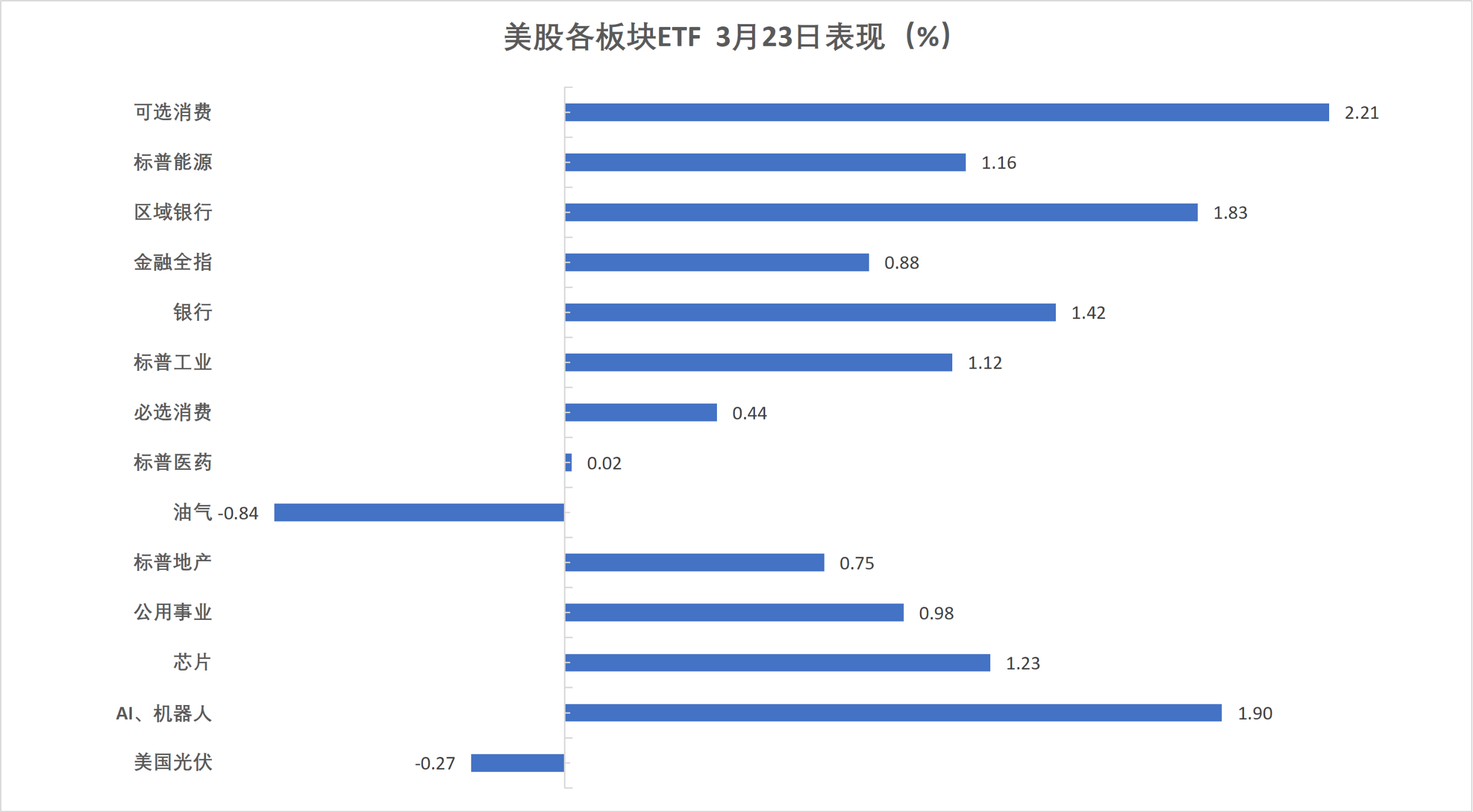

On Monday, the three major U.S. stock indices rose, with the Dow and Nasdaq up less than 1.4%, and small-cap stocks up about 2.3%. Airline ETFs gained nearly 3.5%, leading sector gains. Alaska Airlines and United Airlines shares rose over 4%, American Airlines up 3.66%.

( March 23 U.S. sector ETFs)

March 23 U.S. sector ETFs)

Big Tech:

Semiconductors:

Chinese ADRs:

Other stocks:

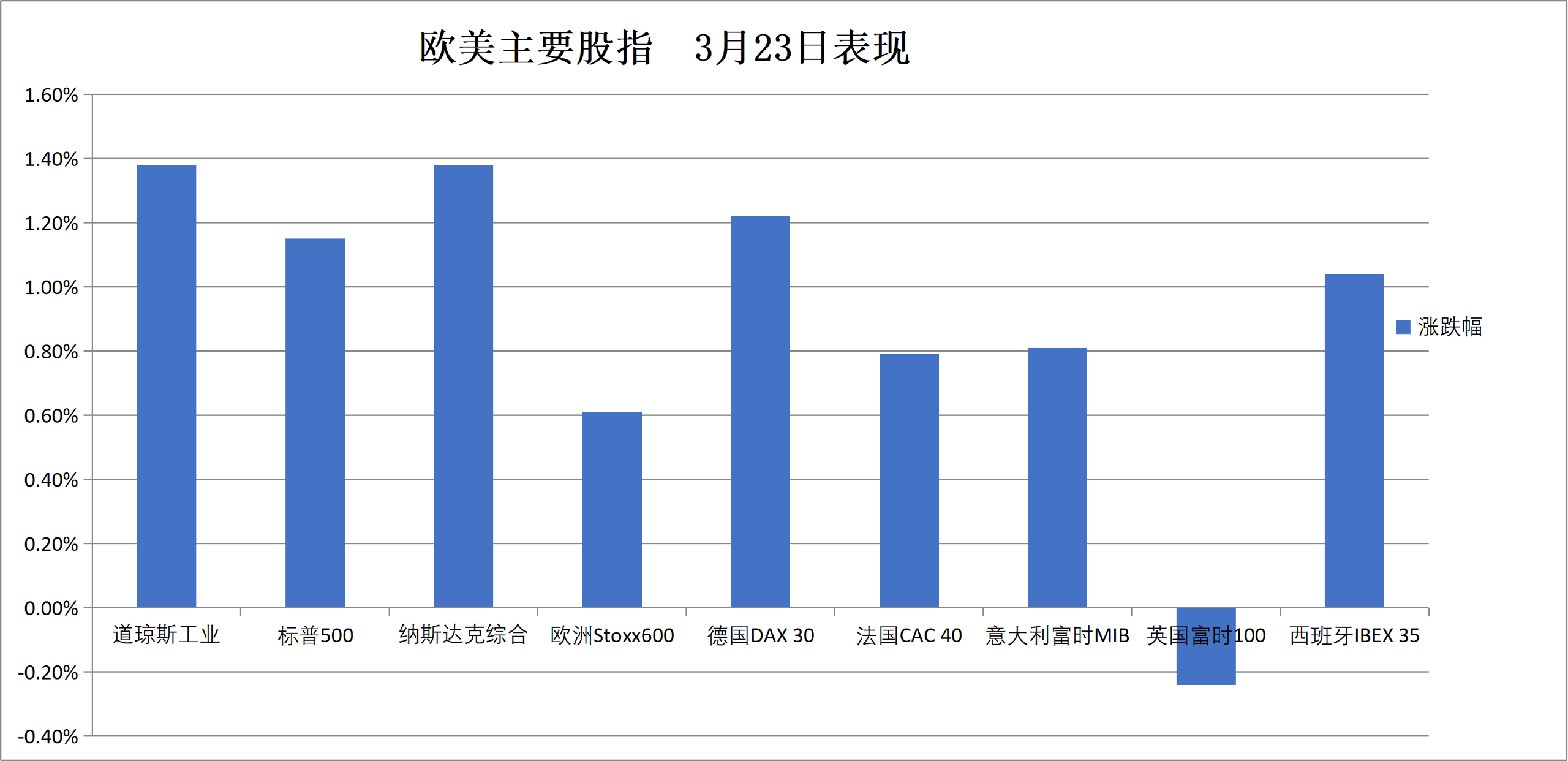

European blue-chip stocks rose over 1.3%, with Siemens Energy up about 4.9%, ASML up about 4.2%. Germany’s DAX up over 1.2%, Italy’s banking sector up over 3.1%, UK stocks down slightly by 0.2%.

Country indices:

( March 23 Major European and US indices)

March 23 Major European and US indices)

Sector and individual stocks:

Two-year German bond yields fell about 10 basis points, UK two-year yields dropped over 15 basis points as investors weigh Trump’s “negotiating with Iran” signals.

( Major U.S. Treasury yields)

Major U.S. Treasury yields)

Eurozone bonds:

The dollar index fell over 0.6%, with the yen briefly strengthening to 158.0. Non-dollar currencies generally appreciated: GBP +0.6%, Hungarian forint and South African rand up over 1.6%, Norwegian krone down over 1.8%.

Non-dollar currencies:

JPY:

Offshore RMB:

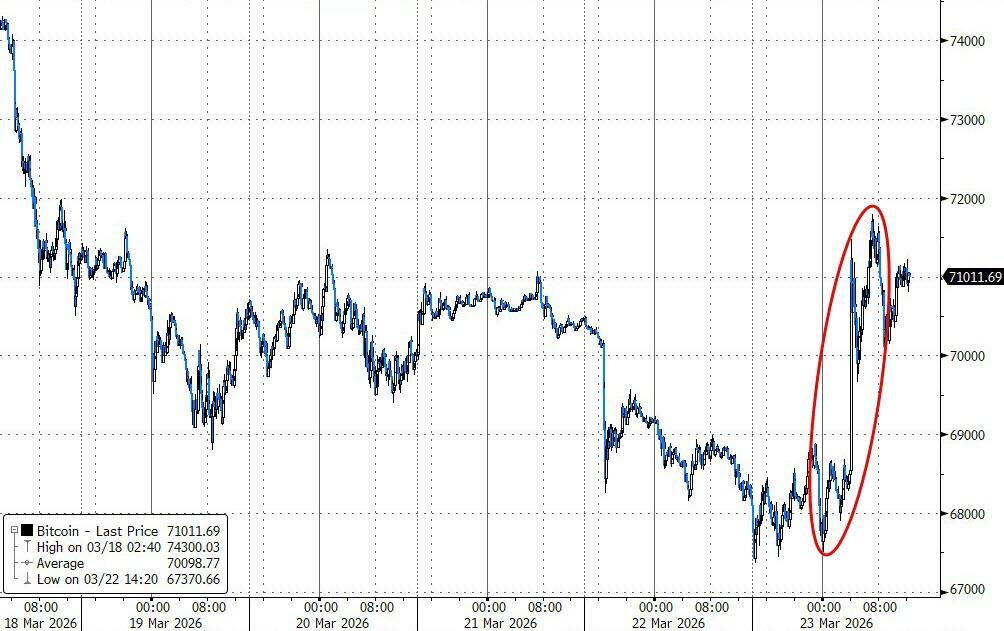

Cryptocurrencies:

( Bitcoin price)

Bitcoin price)

International oil prices fell over 10%, as investors weigh Trump’s claim of “negotiating with Iran.”

( WTI futures)

WTI futures)

Natural Gas:

NY gold futures fell over 3.7%, spot gold briefly dipped below $4,100 before the European markets opened. Spot silver rose 2%, and NY copper futures also gained 2%.

( Gold price)

Gold price)

Silver:

Other metals:

Risk warning and disclaimer

Market risks are inherent; investments should be cautious. This article does not constitute personal investment advice and does not consider individual user’s specific investment goals, financial situation, or needs. Users should determine whether any opinions, views, or conclusions herein are suitable for their circumstances. Investment is at their own risk.