TL;DR

I want to jot down some thoughts I’ve been mulling over—namely, how Bitcoin might perform during a major regime shift in global capital flows, something it has never truly experienced before. I believe that once the shedding phase ends, this could be an incredible trade. In this article, I break down my thinking. Let’s dive in.

What have been the main drivers of Bitcoin’s price historically?

I’m building upon the work of Michael Howell regarding historical drivers of Bitcoin price movements, and using that foundation to better understand how these crosscurrents might evolve in the near future.

As shown in the chart above, BTC’s drivers include:

Since 2021, the simple framework I’ve used to assess risk appetite, gold performance, and global liquidity focuses on the percentage of fiscal deficit relative to GDP. This metric offers a quick read on the fiscal impulse that has dominated global markets since 2021.

A higher fiscal deficit (as a percentage of GDP) mechanically leads to higher inflation, higher nominal GDP, and subsequently, higher total corporate revenues—since revenue is a nominal figure. For businesses capable of leveraging economies of scale, this spells good news for earnings growth.

To a large extent, monetary policy has played a secondary role compared to fiscal stimulus, which has been the primary driver behind risk asset activity. From the chart updated regularly by @BickerinBrattle, it’s evident that monetary impulse in the U.S. is so subdued relative to fiscal policy that I’ll set it aside for now.

As shown in the chart below, we can observe from the data on major developed Western economies that the U.S. fiscal deficit as a percentage of GDP is significantly higher than that of any other country.

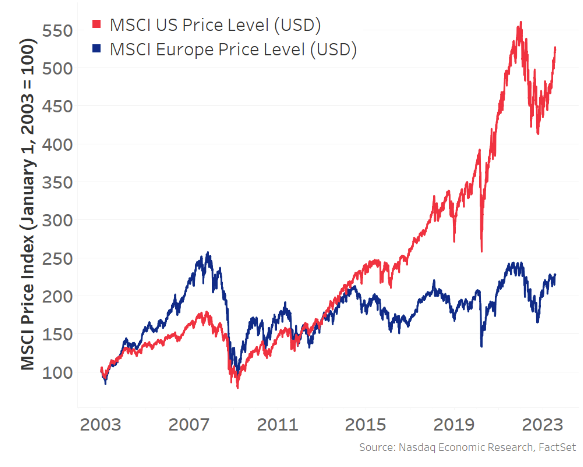

Due to such a large deficit in the U.S., income growth has remained dominant, leading to the U.S. stock market significantly outperforming other modern economies:

This dynamic has made the U.S. stock market a key marginal driver of risk asset growth, the wealth effect, and global liquidity. As a result, the United States has become the most favored destination for global capital flows. This capital inflow dynamic, combined with a massive trade deficit, means the U.S. receives goods in exchange for foreigners receiving dollars, which they then reinvest into dollar-denominated assets (think Treasuries and the MAG7). Thus, the U.S. has become the principal driver of global risk appetite:

Now, circling back to Michael Howell’s work. For over a decade, risk appetite and global liquidity have primarily been driven by the U.S., and this trend has accelerated since the COVID-19 pandemic due to America’s relatively massive fiscal deficits.

Therefore, while Bitcoin is a global liquidity asset (not limited to the U.S.), it has shown a positive correlation with the U.S. stock market, and this relationship has become increasingly pronounced since 2021:c

Now, I believe that this correlation with the U.S. stock market is spurious. When I use the term “spurious correlation” here, I mean it in the statistical sense, because I believe there exists a third causal variable that is not shown in the correlation analysis but is actually the driving force. I argue that this variable is global liquidity, which, as we’ve established above, has been dominated by the U.S. over the past decade.

As we dive deeper into the statistical rabbit hole, we must also establish causation, not just correlation. Fortunately, Michael Howell has done excellent work here as well, using Granger causality tests to establish a causal relationship between global liquidity and Bitcoin.

Can this serve as our starting benchmark?

Bitcoin is primarily driven by global liquidity, and because the United States has consistently been the main engine behind increases in global liquidity, a spurious correlation has emerged.

Now, in the past month, while we’ve all been speculating about Trump’s trade policies and the goals of global capital and orderly liquidity restructuring, a few dominant narratives have surfaced. I categorize them as follows:

The Trump administration wants to reduce trade deficits with other countries. Mechanically, this means fewer dollars flowing abroad, and those dollars would no longer be reinvested into U.S. assets. Without this reduction, the trade deficit cannot shrink.

The Trump administration believes that foreign currencies are being artificially weakened, thereby artificially strengthening the dollar. They aim to rebalance this. In short, a weaker dollar and stronger foreign currencies would result in rising interest rates abroad, prompting capital to return home in search of better rates and domestic equities that benefit from favorable FX adjustments.

Trump’s “shoot first, ask questions later” approach to trade negotiations is prompting the rest of the world—whose fiscal deficits are slim compared to the U.S.—to ramp up government investment in defense, infrastructure, and broad protectionism, striving for greater self-sufficiency. Regardless of whether tariff negotiations de-escalate (with the exception of China), I believe the genie is out of the bottle, and countries will continue pursuing this path.

Trump wants other countries to increase their defense spending as a percentage of GDP and contribute more to NATO, since the U.S. has shouldered a disproportionate burden. This also adds to fiscal deficits.

I’ll set aside my personal views on these ideas—many have been shared already—and instead focus on the logical consequences of these narratives if they continue to play out:

Capital will leave dollar-denominated assets and return home. This means underperformance of U.S. equities relative to the rest of the world, higher bond yields, and a weaker dollar.

This capital is returning to places where fiscal deficits will no longer be constrained. Other modern economies will begin spending and printing to fund these expanded deficits.

As the U.S. continues to shift from a global capital partner to a more protectionist stance, holders of dollar assets will have to start pricing in higher risk premiums associated with these previously “safe” assets and assign them greater margins of safety. When this happens, bond yields will rise, and foreign central banks will seek balance sheet diversification—moving away from pure U.S. Treasuries toward other neutral commodities like gold. Likewise, sovereign wealth funds and pension funds abroad may also pursue greater portfolio diversification.

The counter-narrative is that the U.S. remains the center of innovation and tech-driven growth, and no country is likely to dethrone it. Europe, being too bureaucratic and socialist, cannot pursue capitalism the way the U.S. does. I sympathize with this view. It suggests that this may not be a multi-year trend but rather a medium-term adjustment, since the valuation of these tech names could limit their upside over a certain period.

Returning to the title of this article, The Trade After the Trade, the first trade is selling off the over-owned dollar assets the entire world is heavy on, avoiding the ongoing devaluation. Because these assets are so heavily favored globally, this unwind could turn disorderly as large fund managers and speculative players like multi-strategy hedge funds with tight stop-losses hit their risk limits. When that happens, margin call day arrives—everything gets sold to raise cash. The industry is currently working through this process, preparing its dry powder.

However, as this downward trend stabilizes, the next trade begins—one that features a more diversified portfolio: foreign equities, foreign bonds, gold, commodities, and even Bitcoin.

During these rotation market days and non-margin-call days, we’ve already started to see this dynamic take shape. The dollar index is down, U.S. equities are underperforming, gold is soaring, and Bitcoin has shown surprisingly strong relative performance compared to traditional U.S. tech stocks.

I believe that when this shift occurs, the marginal growth in global liquidity will transition into a dynamic completely opposite from what we’ve been used to. The rest of the world will take on the responsibility of driving increased global liquidity and risk appetite.

As I consider the diversified risks in this global trade war environment, I worry about the tail risks of diving too deeply into foreign risk assets, given the potential for unpleasant tariff headlines that could severely impact those assets. Because of this, in this transition, I view gold and Bitcoin as the cleanest tools for global diversification.

Gold has been in absolute breakout mode, hitting new all-time highs daily, reflecting this regime change. Yet while Bitcoin has performed surprisingly well throughout this shift, its beta correlation with risk appetite has thus far limited its potential—it hasn’t kept pace with gold’s exceptional performance.

So, as we move into global capital rebalancing, I believe the “trade after the trade” is Bitcoin.

When I compare this framework with Howell’s related work, I see the pieces fitting together:

The U.S. stock market is not influenced by global liquidity per se, but by liquidity as measured through fiscal impulse and some capital inflows (which we’ve just established may stop or even reverse). However, Bitcoin is a global asset and reflects a broader view of global liquidity.

As this narrative becomes more defined and risk allocators continue to rebalance, I believe that risk appetite will be driven by the rest of the world, not the U.S.

Gold has already performed exceptionally well, so for the gold-correlated aspect of BTC, that box is checked.

With all this in place, I see for the first time the potential for Bitcoin to decouple from U.S. tech stocks in financial markets. I know—it’s a widow-maker call and often marks Bitcoin’s local tops. But this time, there is real potential for a meaningful shift in capital flows, which could make it sustainable.

So for me, as a risk-seeking macro trader, Bitcoin feels like the cleanest trade after the trade. You can’t tariff Bitcoin. It doesn’t care about borders. It offers high beta exposure for a portfolio without the tail risks currently associated with U.S. tech. I don’t have to bet on the EU getting its act together. And it offers pure exposure to global liquidity—not just U.S. liquidity.

This is precisely the kind of market mechanism Bitcoin was born to serve. Once the dust settles, it’ll be the fastest horse. Accelerate.

Disclaimer:

This article is reprinted from [X]. All copyrights belong to the original author [@fejau_inc]. If there are objections to this reprint, please contact the Gate Learn team, and they will handle it promptly.

Liability Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute any investment advice.

Translations of the article into other languages are done by the Gate Learn team. Unless mentioned, copying, distributing, or plagiarizing the translated articles is prohibited.